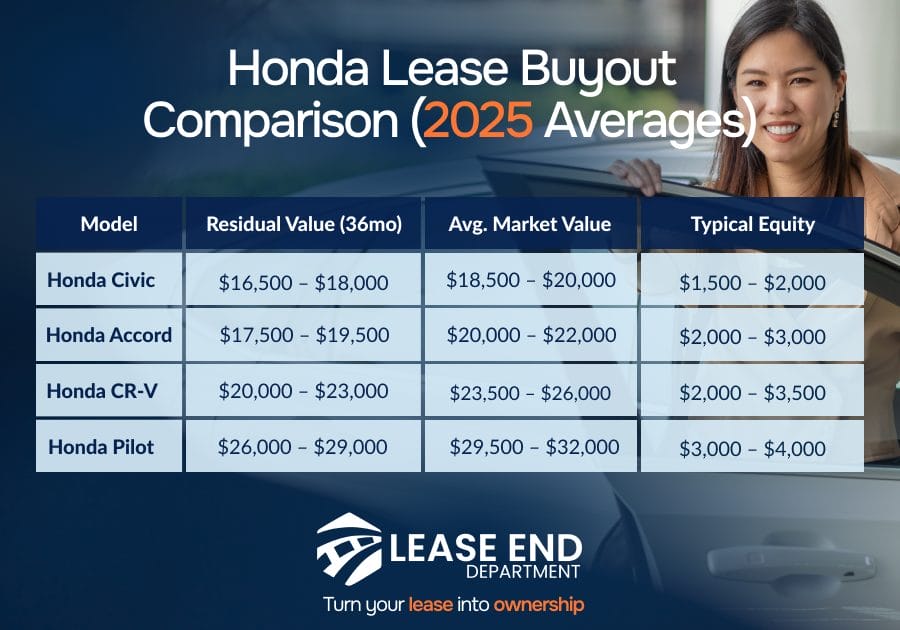

Honda Lease Buyout: Key Takeaways

- A lease buyout lets you buy the car at the end, or even before your lease is up, usually for the price listed in your contract (that’s called the residual value)

- If your car’s worth more than the buyout price, you’ve got equity. That means you could actually save money or even flip it for a profit

- Your total cost to buy the car usually includes the residual value, sales tax, DMV fees, and maybe a paperwork or processing fee, depending on the lender

- Most people don’t pay cash. Financing your buyout is totally normal, with loan terms ranging from 24 to 60 months and interest rates from around 5.5% to 10.5%, depending on your credit

- One big perk of buying the car? You avoid end-of-lease fees, like the $350–$500 disposition charge, or penalties for extra miles or wear and tear

Considering keeping your Honda after the lease ends? You’re not alone.

More than one in four drivers consider buying their leased vehicle, especially when used car prices are high and the car has been well-maintained.

But is a Honda lease buyout the right decision for you?

In this guide, you’ll learn:

- What your Honda lease buyout options actually are

- How to finance the buyout and avoid dealership fees

- What to expect during the process

- Whether buying or returning your car makes better financial sense

Honda Lease Buyout Options To Consider

As your Honda lease comes to an end, you typically have three main options, each with its own pros and cons, depending on your goals and situation.

1. End-of-Lease Buyout

Most drivers opt for this route by completing the lease and then purchasing the car at the price specified in the original agreement.

This option makes sense when:

- The car is in excellent condition

- You’ve stayed within your mileage limit

- Market value is higher than the residual price

Example: If your residual value is $17,500 and similar used Hondas are selling for $20,000, buying the car could save you $2,500 or more.

2. Early Lease Buyout

This option allows you to purchase your Honda before the lease officially ends. You’ll pay the residual value plus any remaining lease payments and possible early termination fees.

It’s a good fit if:

- You’ve exceeded your mileage or anticipate return penalties

- The vehicle’s current value exceeds your payoff amount

- You want to refinance or sell the leased car right away

Pro tip: Use tools like Kelley Blue Book or Edmunds to check your car’s value before making a decision.

3. Third-Party Buyout (If Allowed)

Some leasing contracts allow buyers, such as Carvana or a dealer, to purchase the car directly from Honda Financial Services.

Worth considering when:

- You want to avoid handling the title transfer yourself

- A third-party offer exceeds your payoff quote

- Honda Financial permits third-party sales (always check your contract)

Note: In recent years, some leasing companies have restricted this option, so please confirm your eligibility first.

Honda Lease Buyout Process

Ready to buy your Honda? Here’s how the lease-to-owner process works without the dealership runaround.

Step 1: Get Your Official Payoff Quote

Start by contacting Honda Financial Services or logging into your online account. Request your lease payoff amount, which includes your car’s residual value, plus any remaining fees or taxes.

What you’re looking for:

- Residual value (the pre-set buyout price)

- Sales tax

- Title and registration fees

- Any remaining lease payments (for early buyouts)

Step 2: Check Your Car’s Market Value

Before committing, compare your buyout price to your Honda’s current value.

When checking, you should:

- Use tools like Kelley Blue Book, Edmunds, or Carvana

- See if the market value is higher and if you’ve got equity

- See if the market value is lower, so you can weigh emotional value and condition

Step 3: Decide How You’ll Pay

You can pay in full or finance the buyout with a lease-end loan.

Here’s what to consider:

- Financing is standard as most loans run 24 to 60 months

- Pre-approval helps you avoid dealer markups

- Cash buyers skip interest, but should still compare costs

Step 4: Finalize Ownership

Once paid, the vehicle becomes yours, and you’ll need to wrap up paperwork.

Make sure these final steps are on your to-do list:

- Transfer the title and register the car in your name

- Pay any remaining DMV, plate, and tax fees

- Lease End Department can handle it all 100% online

Pros and Cons of Honda Lease Buyouts

Not sure if buying out your Honda is the right call? Let’s break it down.

Here are the most significant upsides and cons to consider.

Pros

- You already know the car. No surprises. You know its history, how it drives, and how it’s been maintained

- You may have equity. If the market value is higher than your payoff quote, you could save money or sell for a profit

- Avoid lease-end fees. Skip charges for excess mileage, wear-and-tear, or the $350–$500 disposition fee

- No need to shop again. No dealership visits, new lease terms, or sales pressure

- You lock in a set value. And with used car prices jumping all over the place lately, that number might actually work in your favor. It’s one less thing to worry about

One Honda Accord Touring Hybrid driver shared on the myFICO forums that their car’s market value was thousands above the buyout price. Their plan? Keep the caruntil they find a new lease, then flip it and pocket the difference.

Cons

- Higher upfront cost. The buyout amount (plus taxes and fees) can be a financial stretch without financing

- No warranty coverage (in some cases). If your lease is ending, the factory warranty might have expired

- You’re committing long-term. Buying means taking on maintenance, insurance, and resale risk down the line

- Financing might cost more than expected. If you don’t shop around, you could end up with high interest rates or added dealer fees

Honda Lease Buyout Fees and Rates

Buying out your Honda isn’t just about the residual value. There are additional fees and possible finance charges you should add to the total cost.

Here’s what to expect:

Standard Lease Buyout Fees

- The biggest cost is the residual value: That’s the pre-set number in your lease contract. Think of it as the buyout sticker price. Everything else (taxes, DMV, paperwork) stacks on top

- Sales tax: You’ll pay tax on the buyout amount based on your state’s rate

- Title and registration: DMV fees for transferring ownership usually run $100–$400, depending on your location

- Documentation or processing fee: Some dealers charge up to $700 for handling the paperwork

- Disposition fee (if you don’t buy): Around $350–$500, but you avoid this if you complete the buyout

Financing Rates (If You’re Not Paying Cash)

If you plan to finance your Honda lease buyout, lease loan rates vary based on your credit, loan term, and lender:

- Interest rates: Typically between 5.5% and 10.5% in 2025

- Loan terms: Most buyers choose 24 to 60 months

- Monthly payments: Higher than a lease, but you’re working toward full ownership

Pro tip: You don’t have to finance through the dealership. Consider a credit union, your bank, or Lease End Department to secure lower rates and skip extra dealer fees.

How Lease End Department Helps You Buy Out Your Honda

As your Honda lease winds down, you’ve got more options than you think, and we’re here to help you navigate each one with confidence.

At Lease End Department, we help Honda drivers move into ownership without the dealership stress. No pressure, no confusion, just expert support from start to finish.

We make your lease buyout easier with:

- Honest advice and not a sales pitch. We’ll walk you through your lease terms, the value of your Honda, and whether buying it out actually makes sense for you.

- Financing that fits. You can get pre-approved for a loan that works with your credit and budget, no surprise markups or gimmicks.

- All online, all handled. From paperwork to plates, we take care of everything remotely, so you don’t have to deal with dealership lines or DMV visits.

Why Lease End Department? Because we put you in control of your lease-end journey, with no surprises, no sales pressure, and real savings.

FAQs on Honda Lease Buyouts and Financing

Can I buy my Honda before the lease ends?

Yes, that’s called an early lease buyout. You’ll pay the remaining balance plus the residual value and any applicable fees. It may make sense if the car’s market value exceeds the total payoff amount.

How do I know if buying out my Honda is a good deal?

Compare your buyout price (residual value + fees) to your vehicle’s market value using tools like Kelley Blue Book or Carvana. If your car is worth more than the buyout, that’s equity, and a potential win.

Can I finance a Honda lease buyout?

Absolutely. You can apply for a lease buyout loan through a credit union, bank, or Lease End Department. Terms typically range from 24 to 60 months.

Is my residual value negotiable?

In most cases, no. Honda Financial sets the residual value at the start of the lease based on projected depreciation. However, dealerships may offer lease-end incentives or waive minor fees.

What fees will I save by buying my leased Honda?

You’ll skip the disposition fee ( typically $350–$500), and you won’t incur charges for excess mileage or wear and tear, fees that can add up quickly.

Can I return my Honda lease to any dealership?

Yes, but it depends on the dealership’s policies. Most Honda dealerships will accept returns, even if you didn’t lease from them. It’s best to call ahead.