Should You Buy or Return Your Leased Car: Key Takeaways

- Yes, you can buy your leased car, and in today’s market, that might be a smart financial play

- Check the buyout price in your lease contract and compare it to the current value of your car. If your car’s market value is higher, you could gain equity

- Sure, dropping off the car might seem easy, but watch out for sneaky fees like mileage overages, minor dings, or a $400 “thanks-for-playing” return charge

- Lease buyout makes sense if you love the car, drive a lot, or want to skip dealership hassles. It’s yours as you avoid surprise charges and keep a car you already trust

- Start exploring your options 60–90 days before lease-end to avoid rush decisions, limited inventory, or last-minute fees

When your lease is nearing its end, it can feel like you’re at a crossroads: hand over the keys or hang on to the car for good. And for many drivers, the numbers are tipping the scales.

In 2023, the average American drove about 12,200 miles, more than most lease contracts allow per year. That means a lot of people are cruising toward mileage penalties, making the option to buy more appealing than ever.

If you’re weighing whether to return your leased car or buy it outright, you’re in the right place.

In this guide, you’ll learn:

- What your lease-end options really are

- When buying your leased car makes the most financial sense

- What to watch out for if you’re leaning toward returning it

- The key costs, timelines, and fees to plan for

- Real-world advice from drivers who’ve been there

Understanding Your Options at Lease End

Car lease almost up? You’ve basically got different return or lease buyout options, each with its own upsides, costs, and timing quirks.

Here’s what’s typically on the table:

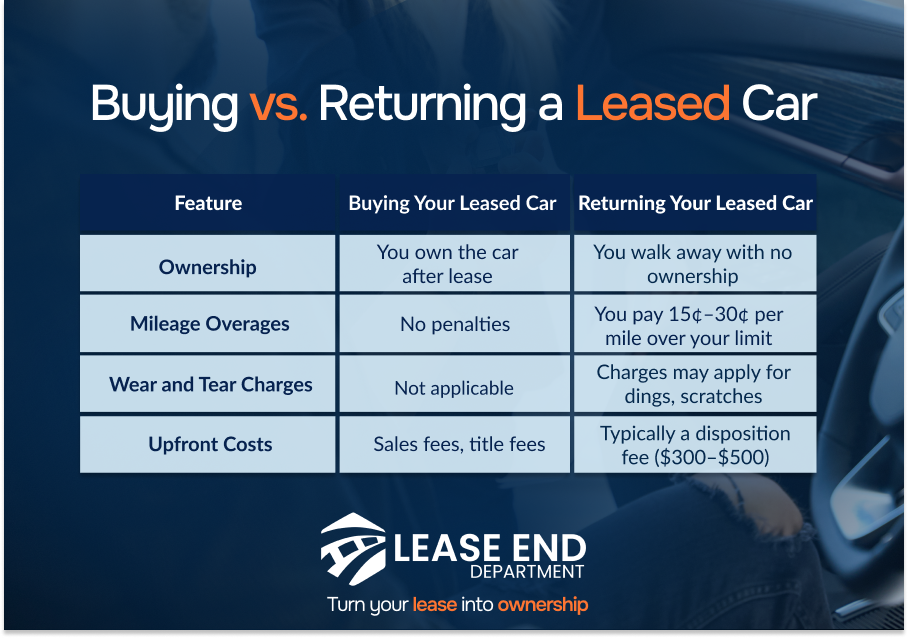

1. Return the Vehicle

This is the default route for many drivers. You hand in the keys and walk away. It sounds simple, but there are a few catches to watch for:

- Disposition fee: Usually $300 to $500, just for returning the car

- Mileage overage: Most leases allow 10,000 to 12,000 miles per year. Go over, and you could pay 15 to 30 cents per extra mile

- Wear and tear: Dents, scratches, or worn tires could trigger repair charges

Pro Tip: Schedule a pre-inspection 30–60 days before lease-end. Fixing small issues ahead of time can save you hundreds.

2. Buy Out the Lease

If the car’s treated you well or you just plain love it, buying it might be your best bet. No guessing games, as you know its benefits, and the price isn’t up for debate.

- You pay the residual value, plus tax and fees

- No mileage or damage penalties apply, because the car becomes yours

- If the car’s worth more than your buyout price, you might even walk away with a little extra value tucked in your pocket

Example: If your buyout price is $17,000 and the car’s market value is $20,000, that’s $3,000 in potential equity.

3. Trade In or Lease a New Car

Want something different? You can return your current lease and roll into a new one, or trade it in and finance a new vehicle.

- Some automakers offer loyalty incentives, like waived fees or reduced rates

- Be sure to compare trade-in offers and double-check whether your current lease has any hidden return conditions

Pros and Cons of Buying Your Leased Car

Not sure whether to buy your leased vehicle? You’re not alone. Many drivers reach the end of a lease and realize the car they’ve been driving still fits their needs and might even be a deal.

Let’s weigh the pros and cons so you can make a confident decision.

Pros of Buying Your Leased Car

- You know the car’s history: No surprises. You know how it drives, how well it’s been maintained, and what to expect down the road

- You avoid excess mileage and wear-and-tear fees: Going over your mileage limit or turning in a car with scuffed wheels or minor dings? Buying skips the penalties

- You could gain equity: If the market value of your vehicle is higher than the buyout price in your contract, you’re in a strong spot. As one forum user put it, “I’m considering buying out my vehicle at the end of my lease in August … the current market value of the car is thousands of dollars above my buy‑out amount.” That’s a textbook example of positive equity in action.

- You’re not starting from scratch: No need to shop for a new car or deal with inflated prices. You already have one you know and trust

Example: If your lease buyout is $17,000 and similar models are selling for $20,000, you’re holding $3,000 in potential equity.

Cons of Buying Your Leased Car

- You’ll need to pay sales tax and registration fees: These vary by state, but can add hundreds to your total cost

- The warranty may be expiring: Most leases cover the factory warranty period. If you buy the car, repairs could soon be on you, unless you add a protection plan. As one Leasehackr forum user put it, “The great thing about a lease is you have those many months to decide if you really like the car or not… You may think you want it for 10 years, but things can pop up about the car, things could break, etc.” It’s a good reminder that long-term ownership comes with long-term surprises.

- Financing might be required: If you don’t have cash on hand, you’ll need a lease buyout loan. Rates vary, and not all dealers offer competitive financing

Pros and Cons of Returning Your Leased Vehicle

If you’re ready for something new or simply don’t want to keep your current car, returning it at lease-end might seem like the easy choice.

But before you drop off the keys, let’s go over what you’re really signing up for.

Pros of Returning Your Leased Car

- No long-term commitment: You walk away clean. No resale process, no loan, and no extended ownership worries

- No new financing required: If your finances are tight or you’re not ready to commit to another vehicle, returning the car lets you pause or reassess

- Opportunity to upgrade: Many automakers offer loyalty perks or lease deals if you stay with the same brand or dealership

Pro tip: Schedule a pre-return inspection 30 to 60 days before your lease ends. This gives you time to fix anything that might trigger a fee, without surprises on return day.

Cons of Returning Your Leased Car

- Disposition fee: Most lease contracts include a return fee, typically between $300 and $500, just for handing the car back

- Wear-and-tear charges: Small dents, scratches, or worn tires? Those could turn into unexpected charges at return time

- Mileage overages: If you drove more than your lease allowed, usually 10,000 to 12,000 miles per year, you may be billed 15 to 30 cents per extra mile.

You may not know that: Over 80% of lease returns include some kind of penalty. From scuffed rims to missing accessories, even minor issues can add up fast.

How Lease End Department Makes Lease-End Easy

Still deciding whether to buy or return your leased car? That’s where we come in.

At Lease End Department, we’re not here to push you into a new car. We’re here to help you make the smartest next move, whether that means turning in the keys, driving off into ownership, or something in between.

Here’s how we make your lease-end experience smoother than a fresh set of tires:

- Buyout support without the dealership runaround: We get your payoff quote straight from the source and show you exactly what it would cost to buy your car

- Financing that fits your budget: Don’t have $18,000 lying around? No problem. We help you explore buyout loan options with pre-approval and no pressure

- We do the paperwork and the DMV lines: You sign online. We handle the title, registration, and even ship your plates to your door

- Friendly, no-fluff guidance: We’re car people and people people. You get real answers, not sales pitches

Whether you’re ready to own the car you’ve come to trust or want to wrap up your lease the smart way, Lease End Department has your back.

Buying or Returning a Leased Car: FAQs

Still have a few questions? Totally normal. Here are some of the things drivers ask most often as they get close to lease‑end.

Should I purchase my leased car?

It depends on your situation, but it often makes sense if your car’s market value is higher than the buyout price, you’ve taken good care of it, or you want to avoid extra fees. Buying also lets you skip the search for a new vehicle and keep a car you already know and trust.

How do I purchase a leased car?

To purchase your leased vehicle, follow these steps:

- Request a payoff quote from your leasing company

- Compare the quote to the market value using online tools

- Decide how to finance it, either pay cash or apply for a lease buyout loan

- Complete paperwork for the title transfer, taxes, and registration

Lease End Department can handle all of this for you, including financing, paperwork, and DMV steps, no dealership visits required.

Can you purchase a leased car before it ends?

Yes, you can. This is called an early lease buyout.

You’ll likely pay:

- The residual value

- Any remaining payments

- Applicable taxes or early termination fees

This option is useful if your car’s value has gone up or if your lifestyle has changed and you want to keep the vehicle long term.

Can I return a leased car early?

Yes, but returning a leased car early often comes with fees. You may owe:

- Early termination penalties

- Remaining payments

- Excess mileage or damage fees

If you’re considering an early return, compare it to an early buyout, you might save money and gain ownership. Lease End Department can help you explore both options with zero pressure.

What happens if I do nothing at lease-end?

If you ignore your lease maturity date, some lenders may automatically extend your lease month-to-month, usually at a higher rate. It’s best to plan 60–90 days in advance to avoid surprise fees or limited choices.

Can I negotiate my lease buyout price?

Usually not as it’s baked into your lease. But if the car’s condition isn’t great or the market dipped, it never hurts to ask. Some lenders may be open to negotiations, especially if they want to avoid processing a return.