Dodge Lease Buyout: Key Takeaways

- A Dodge lease buyout lets you purchase your leased vehicle at the residual value listed in your contract

- Most Dodge leases are financed through Chrysler Capital, which handles payoff quotes and buyout approvals

- Buying your lease can help you avoid mileage penalties, wear-and-tear charges, and dealership markups

- Securing pre-approved financing before visiting a dealership often leads to better loan terms

- Services like Lease End Department can handle the paperwork, title transfer, and financing process

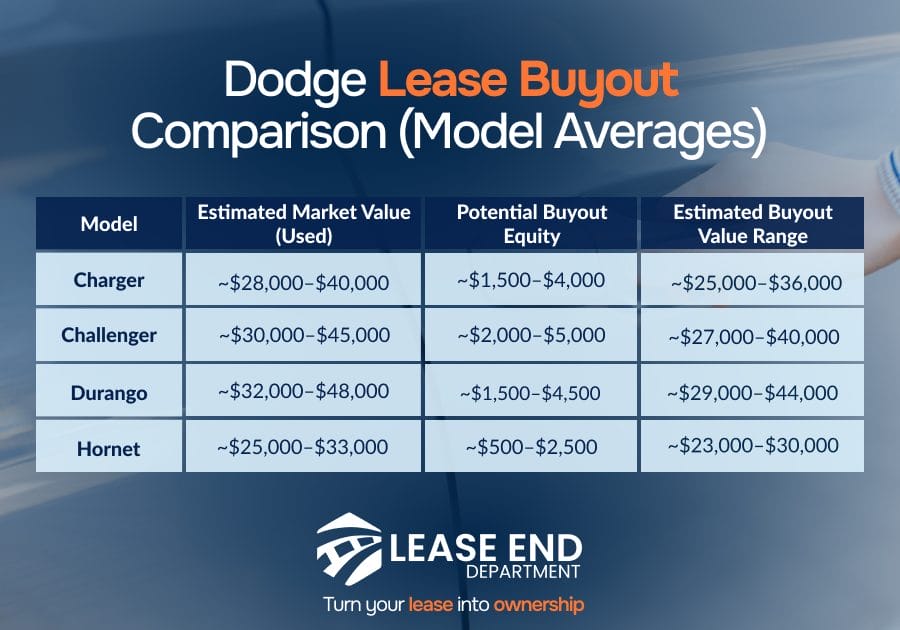

Dodge drivers rarely lease ordinary cars. Vehicles like the Charger, Challenger, and Durango are often chosen for performance, style, and driving experience.

Muscle cars like the Dodge Charger and Challenger often retain 50-70% of their value after 5 years, higher than average sedans.

When the lease term ends, many drivers ask the same question: Should I return the car or keep it?

In many cases, the “keep it” option can be cheaper than buying a similar used car on today’s market.

Here’s what you should know before you decide:

- How a Dodge lease buyout works

- What costs and fees to expect

- How to secure competitive financing rates

- When buying your Dodge lease makes financial sense

- Mistakes to avoid before completing a buyout

What Happens at the End of a Dodge Lease?

Before committing to a buyout, it’s important to understand the three paths available when your Dodge lease ends.

Return the Vehicle

This is the standard option most drivers expect.

You return the vehicle to the dealership. You may need to pay:

- A disposition fee (often $300–$500)

- Mileage overage charges

- Wear-and-tear fees

Lease Another Dodge

Some drivers choose to upgrade to a new model.

Manufacturers sometimes offer:

- Loyalty incentives

- Fee waivers

- Reduced down payments on new leases

Buy Out Your Current Dodge

This option allows you to keep the vehicle you already drive.

Instead of returning the car, you purchase it by paying the residual value plus applicable fees and taxes.

For many drivers, this becomes the most affordable option.

How the Dodge Lease Buyout Process Works

Buying out your Dodge lease is usually straightforward, especially if you start the process before your lease officially ends.

Most Dodge leases are handled through Chrysler Capital, but the overall steps are similar regardless of the lender.

Step 1: Request Your Lease Payoff Quote

Start by requesting your lease payoff quote from your leasing company, usually Chrysler Capital.

The quote shows the total cost to purchase your vehicle and typically includes:

- Residual value from your lease contract

- Remaining lease payments (if buying early)

- Sales tax

- Administrative or purchase fees

Pro Tip: Always request the payoff directly from the leasing company to avoid dealership markups.

Step 2: Compare the Payoff to the Vehicle’s Market Value

Next, check what your Dodge is worth on the used car market.

You can estimate the value using tools like:

- Kelley Blue Book

- Edmunds

- CarMax or Carvana offers

If the vehicle’s market value is higher than the buyout price, you may have positive equity.

Step 3: Choose the Right Buyout Timing

You can buy out your Dodge lease either at the end of the lease term or before it ends.

End-of-lease buyout

- Happens when your lease finishes

- Usually the simplest option

- Early lease buyout

- Occurs before the lease ends

- May include remaining payments or additional fees

Step 4: Finalize Financing

Once you decide to move forward, you can either pay cash for the buyout or finance it with a lease buyout loan. Many drivers compare rates from banks, credit unions, or lease buyout specialists to find the most competitive terms.

After financing or payment is arranged, the final step is completing the paperwork and transferring ownership.

This includes signing purchase documents, transferring the vehicle title, and registering the car in your name through the DMV. Once these steps are finished, your leased Dodge officially becomes your owned vehicle.

Dodge Lease Buyout Costs, Fees, and Taxes

Before buying out your Dodge lease, it’s important to understand the total cost of the purchase, not just the residual value listed in your contract. The final price usually includes taxes, administrative fees, and registration costs.

Here are the most common expenses drivers encounter during a Dodge lease buyout.

Residual Value

The residual value is the pre-determined price you can pay to purchase the vehicle at the end of the lease.

This number is set when you sign the lease and is based on the expected depreciation of the vehicle.

For most Dodge vehicles, the residual value is typically 50–60% of the original MSRP after a three-year lease.

Example:

- Original MSRP: $40,000

- Residual value after three years: $22,000

This amount forms the base price of your lease buyout.

Purchase Option Fee

Most leasing companies charge a purchase option fee when you buy the vehicle at lease-end.

This administrative charge usually ranges from $300 to $500, depending on the lender.

For Dodge leases financed through Chrysler Capital, this fee is typically included in your payoff quote.

Sales Tax

Sales tax is applied to the buyout price of the vehicle in most states.

Tax rates vary by location, but they typically fall between 6% and 10% of the purchase price.

Example:

- Buyout price: $22,000

- Sales tax (7%): $1,540

- Total purchase price: $23,540 before additional fees.

Title and Registration Fees

After completing the buyout, you’ll need to register the vehicle in your name and transfer the title.

These DMV-related costs usually range from $150 to $400, depending on your state.

This step officially converts the vehicle from a leased asset into your personal property.

Early Buyout Costs (If Applicable)

If you choose to buy out your Dodge lease before the term ends, the payoff amount may include additional charges such as:

- Remaining monthly lease payments

- Early termination or processing fees

- Applicable taxes and administrative costs

Because of these added costs, early buyouts are usually worthwhile only if the vehicle’s market value is significantly higher than the payoff amount.

Example Dodge Lease Buyout Calculation

Here’s a simple example of how the numbers may look for a Dodge lease buyout:

- 2021 Dodge Charger

- Residual value: $24,000

- Purchase option fee: $400

- Sales tax (7%): $1,680

- Title and registration: $250

- Estimated total buyout price: $26,300

Common Dodge Lease Buyout Mistakes to Avoid

Avoiding a few common mistakes can help you make a more confident and financially sound decision.

Not Comparing the Buyout Price to Market Value

One of the most common mistakes is assuming the lease buyout price is automatically a good deal.

While the residual value is fixed in your contract, the used car market constantly changes. If your Dodge Charger, Challenger, or Durango is worth less than the buyout price, purchasing it may not make financial sense.

Before committing to a buyout, check your vehicle’s current value using tools like Kelley Blue Book, Edmunds, or CarMax. This quick step helps confirm whether the buyout price is competitive.

Waiting Until the Last Minute

Many drivers only start considering a lease buyout during the final weeks of their lease, which limits their options.

Waiting too long can lead to rushed decisions, fewer financing choices, and pressure to accept dealership loan offers.

Starting the process 60–90 days before your lease ends gives you time to compare lenders, review your payoff quote, and plan the next step without pressure.

Accepting Dealer Financing Without Comparing Rates

Dealerships often offer financing for lease buyouts, but those loans are not always the most competitive option.

Some dealer loans include higher interest rates or hidden markups, which increase your total loan cost over time.

Comparing offers from banks, credit unions, or lease buyout specialists can often result in better terms and lower monthly payments.

Forgetting to Budget for Taxes and Fees

Another mistake is focusing only on the residual value while ignoring the additional costs involved in the buyout.

In most states, you will also need to pay sales tax, title transfer fees, and registration costs. These charges can add thousands of dollars to the total purchase price if you are not prepared for them.

Understanding the full cost upfront helps you avoid surprises and plan your financing more accurately.

Keep Your Dodge Without the Dealership Hassle With Lease End Department

Reaching the end of your Dodge lease does not mean you have to give up a vehicle you already enjoy driving.

A lease buyout can be a smart way to transition from leasing to ownership, especially if the buyout price is competitive and the car still fits your lifestyle.

However, the process can feel complicated when you factor in payoff quotes, financing, taxes, and title transfers. That’s where Lease End Department helps make the transition simple.

Why drivers choose Lease End Department:

- Skip the dealership: Complete your lease buyout without negotiating with a dealership

- Competitive financing options: Compare rates from trusted lenders to find a payment that fits your budget

- Full paperwork support: We handle title transfer, registration, and DMV documentation

- Transparent numbers: See your buyout costs clearly before making a decision

- A faster, simpler process: Everything can be completed online or over the phone

Besides Dodge, we also specialize in lease buyouts for additional popular brands, including:

With the right support, keeping your Dodge can be easier than starting over with a new lease or loan.

Dodge Lease Buyout FAQs

Can you buy out a Dodge lease early?

Yes, most Dodge leases allow an early buyout. The payoff amount usually includes the residual value plus any remaining payments and applicable fees.

How do I get my Dodge lease payoff amount?

You can request your payoff quote directly from Chrysler Capital or your leasing company. The quote shows the total cost to purchase your leased Dodge, including taxes and administrative fees.

Is a Dodge lease buyout worth it?

It may be worth it if the vehicle’s market value is higher than the buyout price or if you want to keep a car you already know and trust. Comparing your payoff quote to current resale values can help you decide.

Do you pay sales tax on a Dodge lease buyout?

Yes, most states charge sales tax on the buyout price. You may also need to pay title transfer and registration fees when completing the purchase.

Can you negotiate a Dodge lease buyout price?

In most cases, no. The buyout price is based on the residual value set in your lease contract, though you can still compare financing options to reduce the overall cost.

What happens at the end of a Dodge lease?

At the end of a Dodge lease, you typically have three options: return the vehicle, lease another car, or buy out your current lease. Your lease agreement will outline the residual value and any potential end-of-lease fees.

How far in advance should I plan my Dodge lease end?

It’s best to start reviewing your options about 60–90 days before your lease ends. This gives you time to compare buyout costs, schedule inspections, and explore financing if you plan to keep the vehicle.