GM Lease Buyout: Key Takeaways

- Your GM lease buyout price is pre-set, but your timing determines the value. The wisdom of acting early or at lease-end depends on mileage, condition, and resale trends

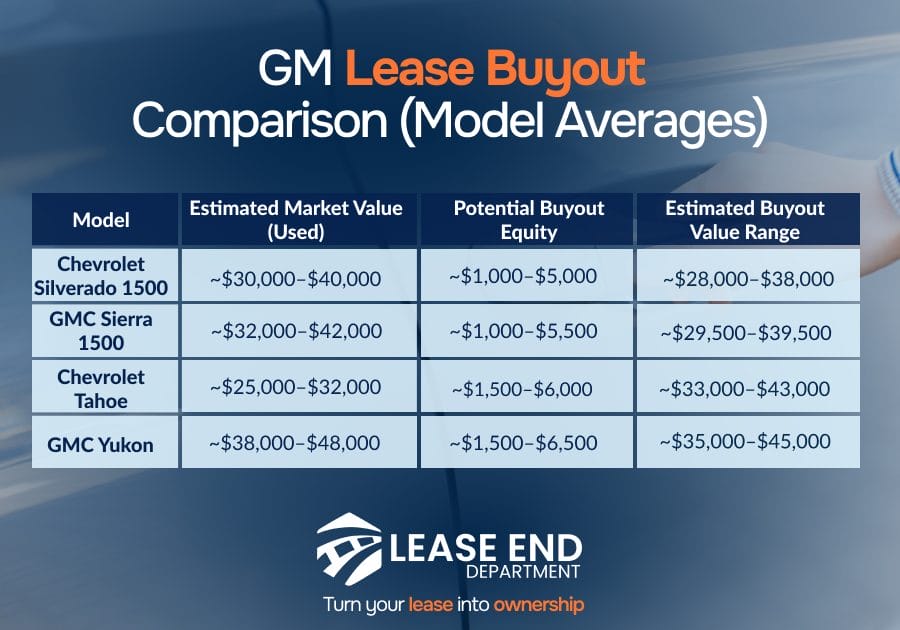

- Trucks and SUVs like the Silverado, Tahoe, and Yukon often hold equity. If your market value is higher than your payoff, that difference belongs to you

- The dealership doesn’t need to control your buyout. You can skip the upsells and markups by going directly through GM Financial or Lease End Department

- Taxes and fees can add thousands to your total cost. Don’t just look at the residual, factor in sales tax, title, registration, and purchase fees

- You already know the vehicle, now make it yours without surprises. A smart buyout is about more than price. It’s about trust, timing, and keeping what works

When your GM lease is coming to an end, deciding whether to keep it or return it usually comes down to numbers, not emotion.

You already know how the vehicle drives. You know its service history. What you may not know is whether buying it makes financial sense right now.

In some cases, it does. In others, it doesn’t. The difference? Market value, mileage, and timing.

Full-size GM trucks and SUVs often retain a solid portion of their value, sometimes landing in the mid-50% to mid-60% range after five years depending on condition and demand. That can create a situation where the buyout price is lower than current resale value.

When that happens, you may have equity.

Below is a practical breakdown of:

- How the GM lease buyout process works, step by step

- What it costs, including taxes, fees, and early buyout scenarios

- The best financing options for GM trucks and SUVs

- Pros, cons, and the equity question: should you buy it or walk away?

- Examples to help you skip the dealership drama and decide better

Should You Keep Your GM Truck or SUV?

Deciding whether to keep your vehicle starts with a few practical questions:

- Has the vehicle held its value well?

- Is your mileage below the lease allowance?

- Would replacing it cost more in today’s market?

Besides these starting questions, you should also consider:

- Residual vs. resale: GM models like the GMC Sierra, GMC Yukon, and Chevrolet Tahoe often retain around 60% of their original value after five years

- Lease-end risks: Returning the vehicle may come with over-mileage charges, excess wear fees, or limited incentives to lease again

- Avoid the dealership cycle: Buying out lets you skip dealer markups and hold on to a vehicle that’s already road-tested and reliable

Chevy Tahoe Equity Opportunity Example

- Vehicle: 2020 Chevrolet Tahoe

- Original MSRP: $56,000

- Residual value (buyout price): $32,000

- Current market value (2024): $36,500

- Equity if you buy it out: $4,500

That $4,500 could be applied as trade-in value later or saved as equity. Either way, it’s yours if you buy smart.

Comparing Your Options: Return, Replace, or Buy Out?

When your lease ends, you generally have three lease buyout or return options to consider.

Whether you hand back the keys, roll into something new, or keep what you’ve got, each path has its trade-offs.

If You Decide to Hand the Vehicle Back

Sometimes the cleanest break is just that: a clean break. But it’s rarely cost-free.

- You’ll schedule a lease-end inspection through GM Financial

- Expect fees for excess mileage or wear-and-tear (even minor dings count)

- You walk away with no car, no equity, and potentially no incentives

Tip: If you’re over mileage or your GM is in great condition, this option could leave money on the table.

If You’re Thinking About Starting a New Lease

If you love the new-car cycle, this may be tempting, but it has its price.

- Some lessees qualify for loyalty or pull-ahead incentives

- Monthly payments may be higher, especially with rising vehicle prices

- You’re resetting the clock: no ownership, no equity

If you decide on a new lease, consider: Do you want another round of leasing, or is it time to build value through ownership?

If Keeping the Vehicle Makes More Sense

The car fits. You know its advantages. And you might be buying it for less than it’s worth.

- Keep equity if market value exceeds your payoff

- No guesswork, you already know the service history and condition

- Avoid dealership pressure, new-car markups, and financing games

If your truck’s resale value is $5,000 above its residual, that’s your leverage, whether you keep, trade, or sell your leased car.

How the GM Lease Buyout Process Actually Works

Ownership begins with understanding the numbers in your car lease agreement.

Once you see the full picture, the steps fall into place.

Request Your Payoff Quote

The first step is requesting your payoff amount from GM Financial.

- Request your payoff quote directly from GM Financial, online or by phone

- Your quote includes the residual value, applicable taxes, and buyout fees

- Ask whether any early termination costs apply if you’re buying before lease-end

A 2020 GMC Sierra with a $52,000 MSRP may show a residual around $28,000, with a total payoff closer to $30,500-$31,000 once fees and tax are included.

Compare Your Payoff to Market Pricing

Once you have the number, check what similar vehicles are selling for.

- Check current values using Kelley Blue Book, Edmunds, CarMax, and Carvana

- If resale value is higher than your payoff, you’re looking at positive equity

- Compare trim carefully. A decked-out Z71, Denali, or AT4 can be worth thousands more than a base model

Trim packages, drivetrain options, and mileage can shift resale values by $1,000-$3,000 or more. Never rely on a single estimate.

Decide on Timing

Buying the right vehicle at the wrong time can cost you just as much as a bad deal.

- Early buyouts may include fees, but can help you avoid excess mileage or wear charges

- Lease-end buyouts are simpler, but often come with dealership pressure to upgrade

- If demand is strong for your model, buying earlier can lock in equity while prices are high

In practice, many drivers choose to buy GM trucks and SUV early to avoid mileage penalties and capitalize on resale demand.

Pay or Finance to Finalize Ownership

This is where ownership becomes official and control shifts fully into your hands.

- Paying cash avoids interest, but be sure to account for taxes and registration

- Financing spreads out the cost and preserves liquidity

- Lease End Department offers online pre-approvals with no dealership markup

- LED can manage title transfer, taxes, registration, and plates from start to finish

Financing the full GM lease buyout amount, including taxes and fees, can keep cash available while moving you into ownership.

GM Lease Buyout Costs, Fees, and Taxes

Before you decide to keep your truck or SUV, get a full view of what the buyout will really cost.

Use this table to break it down:

| Cost type | Estimated range | Notes |

| Residual value | 50%–60% of MSRP | Locked in at lease signing. For a $60,000 Yukon, that’s ~$30,000–$36,000. |

| Sales tax | 6%–10% of buyout price | Based on your state. Add $1,800–$3,000 on a $30,000 payoff. |

| Purchase option fee | $300–$500 | Usually listed in your lease contract. Often non-negotiable. |

| Title & registration | $150–$400 | Higher for heavier or commercial-rated trucks/SUVs. |

| Early termination fee | Up to remaining payments | Applies only if buying out before lease end. Check your contract. |

Most drivers forget to budget for taxes and title, which can add $2,000+ to your final buyout amount, especially on large GM vehicles like the Tahoe, Sierra, or Suburban.

Financing a GM Lease Buyout Without the Dealership

Not all financing is created equal, and dealership options often come with strings attached. Here’s how to navigate the smarter route.

Why Dealership Financing Isn’t Always Best

Sometimes the most expensive part of a lease buyout isn’t the car. It’s the fine print.

- Dealerships may mark up interest rates compared to third-party lenders

- You’ll likely face sales pressure to lease or buy new, not keep your current truck or SUV

- Financing terms may be rigid, especially for off-lease vehicles

Why Third-Party Lenders Like Lease End Department Work Better

You’re not buying a new car. You’re buying the one you already know, and your lender should treat it that way.

- Fast online pre-approvals without the showroom shuffle

- Rates designed for off-lease and used vehicles

- No hidden markups, no upgrade talk, just clear buyout financing

Example: A $32,000 buyout financed over 60 months at 6.5% APR = ~$598/month. (That’s before taxes and title, but yes, you can finance those too.)

Mistakes GM Lessees Make and How to Avoid Them

A GM lease buyout is a financial opportunity. But rushing or relying on outdated advice can turn a good deal into a missed one.

A few common issues to consider:

- Don’t wait until the last month: Delays can limit financing options and put you at the mercy of dealership deadlines

- Don’t assume you need the dealership: Buyouts go through GM Financial, not the lot where you leased. You’re in control

- Don’t skip the resale check: Use KBB, Edmunds, Carvana, and CarMax. Equity happens when your vehicle’s value beats the payoff

- Don’t ignore fees and taxes: They can add $2,000+ on a full-size GM truck or SUV

- Don’t buy without a plan: If your warranty’s expired or you plan to trade soon, think strategically, not emotionally

How Lease End Department Helps You With GM Lease Buyout

If you prefer not to complete the transaction through a dealership, turn to third-party services that specialize in lease buyouts.

Lease End Department is one example that focuses specifically on off-lease vehicles and processes transactions digitally.

Here’s what we offer:

- Instant access to your GM payoff details with residual, taxes, and fees all explained

- Buyout financing made easy as you get re-approvals in minutes, with competitive rates tailored for off-lease trucks and SUVs

- Full-service paperwork: From title transfer to registration and DMV processing, we handle the details so you don’t have to

- No dealership pressure: no upsells, hidden fees, or markups

- Fast, digital-first experience as you complete everything online, including plate delivery

- Support from real humans: Our team is here to walk you through every step if you need help

Besides Volkswagen, we also specialize in lease buyouts for additional popular brands, including:

GM Lease Buyout: FAQs

If you’re considering a GM lease buyout, this information can help clarify the process.

What is a GM lease buyout?

A GM lease buyout allows you to purchase your leased Chevrolet, GMC, Buick, or Cadillac vehicle at the end of the lease or earlier based on the residual value set in your contract.

How do I buy out my GM lease?

You can buy out your GM lease by requesting a payoff quote from GM Financial, comparing it to your vehicle’s market value, securing financing or paying in cash, and completing the title and registration transfer.

Can I buy my GM vehicle before the lease ends?

Yes, GM Financial allows early GM lease buyouts. You’ll need to pay the remaining lease balance, residual value, and any applicable fees. Early buyouts can help avoid mileage penalties or excess wear-and-tear charges.

What fees are included in a GM lease buyout?

Typical GM lease buyout costs include the residual value, sales tax (6–10%), a purchase option fee ($300–$500), title and registration fees ($150–$400), and potentially early termination fees if you’re buying before lease-end.

Does GM Financial offer financing for GM lease buyouts?

GM Financial may not always offer lease-end financing. Many drivers use third-party options like Lease End Department for faster approvals, competitive rates, and no dealer markups.

Can I get equity from my leased GM truck or SUV?

Yes. If your vehicle’s current market value is higher than your lease buyout price, you may have equity. This equity can be used as trade-in value, refinancing leverage, or instant resale profit.